Fronting Felsy, $5000 opportunity, scale back frenzy, Chaser cameo, Asciano, Rich List and much more

July 16, 2009

Dear Mayne Reporters,

It's been another big week with five speeches, lots of capital raising plays, an apperance before the Productivity Commission inquiry into executive pay and even a cameo appearance on The Chaser, which gave us the excuse to put together this lively video about our combative but good natured history with the boys:

The full edition is choc-full of lively material and available online here. It includes some easy advice to potentially make a quick $5000 out of Macquarie Bank in a story that Crikey, for some inexplicable reason, declined to run today. Have a read, get set and then send the link to all your friends.

It's been another big week with five speeches, lots of capital raising plays, an apperance before the Productivity Commission inquiry into executive pay and even a cameo appearance on The Chaser, which gave us the excuse to put together this lively video about our combative but good natured history with the boys:

The full edition is choc-full of lively material and available online here. It includes some easy advice to potentially make a quick $5000 out of Macquarie Bank in a story that Crikey, for some inexplicable reason, declined to run today. Have a read, get set and then send the link to all your friends.

Spread the message on some easy money

Crikey declined to run the following story on Friday which was disappointing because it pulls together much of what is wrong with Australia's cowboy system of capital raisings and also presents an arbitrage opportunity in Macquarie Leisure that will no doubt be swamped as the word gets out. You may as well all get on board, but remember the issue will probably be heavily scaled back. Also, the stock will probably fall back by the middle of next week because small punters are pouring in. As at 2pm on Friday there had been 2068 trades in a stock that only has 7000 shareholders and by close of business it reached a whopping 3683. The average trade has been less than 2000 shares so it really is being dominated by retail opportunists and will continue that way on Monday. Anyway here's the Crikey contribution which never saw the light of day:

Macquarie dunderheads leave the door open

Crikey founder Stephen Mayne writes:

Want to make a leisurely $5000 in a few weeks? Buy $500 worth of shares in Macquarie Leisure (ASX code: MLE) before close of trade on Monday and you're in with a shot.

The Millionaires Factory and the Macquarie Leisure board have shown themselves to be complete dills in the way they've structured the management internalisation and capital raising announced yesterday.

First up, they've done a highly dilutive $41.7 million share placement at only $1.15 each. Surely the board knew that the shares would be re-rated once the $3-5 million fee leakage to Macquarie each year had been eliminated.

Sure enough Macquarie Leisure shares jumped 15c to $1.50 when trade resumed this morning and the board announced that the selective placement to the big end of town was “significantly over-subscribed”.

No wonder, these lucky clients of under-writers Macquarie and RBS have made a paper profit of more than $10 million. Where was the price tension? Where was the book build to minimise dilution?

The existing Macquarie Leisure shareholders will be further diluted because the dunderheads have announced a $15,000 share purchase plan for retail investors with a record date of next Thursday, July 2.

Therefore, anyone who buys $500 worth of shares before close of trading on Monday will qualify to apply for $15,000 worth of shares in the SPP at only $1.15 a pop.

I was already on the register but the wife, another relative and an employee have each bought another $500 worth this morning meaning we'll be collectively stumping up $60,000 in an attempt to make a quick $20,000 profit.

However, as was explained in this piece for the Fairfax websites on June 23, the only problem is that thousands of other opportunists and day traders will jump on the arbitrage, especially now that the secret is being shared with the vast Crikey army. (Well, actually no, they declined to run the story!)

It's money for jam and this is what one UBS adviser sent to all his clients today:

We have become aware of a small arbitrage opportunity in MLE which are currently in the process of issuing shares as part of a share purchase plan (capital raising). Shareholders have the right to purchase up to $15,000 worth of shares at $1.15 which equates to approximately 13,000 units. Providing the share price holds (currently $1.50) for the period of the offer, this represents a profit of $5,000 or 30.0% on an investment of $15,000.

Macquarie Leisure has said there is only $18.3 million available for the SPP, so it is likely to be massively over-subscribed and heavily scaled back.

Macquarie Leisure CEO Greg Shaw said the company only had 7000 retail shareholders and adding a few more in the next two trading days would boost liquidity and turnover which in turn could help the stock make the ASX200.

Whilst Shaw admitted that “obviously this is an opportunity for some people to take up”, he claimed the board “was not actively encouraging it”.

Yeah, but we are Greg and with the ability to spread news fast online, you are going to see thousands of new Macquarie Leisure shareholders buy before Monday's deadline.

Assuming Macquarie Leisure finishes with 10,000 eligible shareholder on board by next Thursday's record date, that's a potential $150 million worth of applications chasing $18.3 million, so the scale back will probably be huge.

Finally, check out this list of other companies which have left the gate open for opportunists during the record breaking run of heavily discounted capital raisings.

It just shouldn't happen and who would have thought the Millionaires Factory would join the club. Indeed, it would be interesting to know if Macquarie Bank employees are allowed to join in the party, all of which is being funded by the existing Macquarie Leisure shareholders who suffer completely unnecessary dilution.

Some bouquets for Macquarie Leisure directors

Leaving aside all those brickbats on what is ultimately a fairly immaterial issue in financial terms, the non-executive directors of Macquarie Leisure, led by Anne Keating and chairman Neil Balnaves, are to be congratulated for successfully breaking free of the Millionaires Factory.

Macquarie obviously drove a hard bargain extracting $17 million for its management contract, but I understand the whole process was actually driven by the independent directors who took their responsibilities seriously. Macquarie didn't seek or particularly want the deal and negotiated in their usual aggressive way.

Anyone who thinks this automatically means Macquarie Airports and Macquarie Infrastructure Group will go the same way ought to look at just who are the independent directors on those boards.

MAP in particular is stacked with Macquarie partisans and Bermudan box tickers, whilst MIG features Leighton chairman David Mortimer, who used to have his office at Macquarie. If only MIG and MAP followed the Macquarie Leisure by having an independent chairman, rather than Mark Johnson and Max Moore-Wilton respectively.

The best thing about Macquarie Leisure's internalisation proposal is that CEO Greg Shaw will now actually work for the directors and the shareholders, rather than being employed by Macquarie on a salary that has never been disclosed.

Fronting Felsy and friends at the PC pay inquiry

Canberra fog delayed the start of the Melbourne hearings of the Productivity Commission's executive pay inquiry so a one hour appearance for your correspondent scheduled to commence at 9.30am on Wednesday turned into a lively 70-minute exchange starting at 12.10pm.

The three commissioners had only been furnished with this original two-page submission so the delay provided the extra two hours necessary to come up with another two pages to present on the day. Some of that material is reproduced below. The key message was that we need to fix the system of director elections in Australia and to demonstrate the problem the following was produced:

Biggest remuneration report protest - why back the directors?

This list tracks the 13 protest votes exceeding 40% against remunerations reports at ASX200 companies since 2006 and shows how the unidentified institutional shareholders backed the directors at the same AGMs who got the pay policies wrong. If you vote against remuneration reports, surely you should vote against the responsible directors.

Valad Property Group, 2008: 76.1% against rem - big bonuses as company close to collapse.

Least popular director: Bob Seidler, 85.8% in favour

Telstra, 2007: 66.18% against rem - not enough performance hurdles or disclosure for Sol Trujillo.

No directors up for election.

AGL, 2007: 62.56% against rem – CEO Paul Anthony pocketed $17 million for 17 months work.

Least popular director: chairman Mark Johnson: 83.2% in favour

Transurban, 2008: 58.56% against rem - $16.6 million farewell to former CEO Kim Edwards.

Least popular director: chairman David Ryan, only 57.1% in favour due to ABC Learning baggage.

Boral, 2008: 58% against rem - big increase in base pay and short term bonuses for CEO Rod Pearce.

Least popular director: Paul Rayner, 99.5% in favour

Wesfarmers, 2008: 50.50% against rem - poor disclosure of incentive scheme for CEO Richard Goyder.

Least popular director: chairman Bob Every, 99.5% in favour

Oxiana, 2006: 46.9% against rem - changed the performance period on CEO Owen Hegarty's options.

Least popular director: Michael Eager, 99.3% in favour

Alumina, 2007: 46.2% against rem - CEO incentives not structured appropriately.

Least popular director: Peter Hay, 99.2% in favour

MFS, 2007: 45.92% against rem - options for chair Andrew Peacock and excessive cash for executives.

Least popular director: Paul Manka, 99.2% in favour

Toll Holdings, 2008: 42.94% against rem - big protest against $55m options buyout in Asciano demerger.

Least popular director: chairman Ray Horsburgh: 99.7% in favour

Qantas, 2008, 41.48% against rem – Geoff Dixon highest paid airline CEO in the world.

Least popular director: Barbara Ward: 59% in favour

Zinifex, 2006: 41.26% against rem - excessive $12 million incentive payment to outgoing CEO Greg Gailey.

Least popular director: Tony Larkin, 99.9% in favour

Suncorp, 2007: 40.61% against rem - excessive incentive payments guaranteed after Promina takeover.

Least popular director: Dr Cherrell Hirst, 98% in favour.

Fix corporate voting, especially the no vacancy rort

The key to corporate governance, including executive pay, is fixing up the director election system. The biggest problem is where boards require a challenger to knock off an incumbent to get elected by declaring there is “no vacancy”. The average incumbent gets 96% in favour and when you throw in the typical 10% of the vote as undirected proxies in the chairman's back pocket, it was statistically impossible for me to get elected in the majority of 35 board tilts. 100% of directed proxies in favour would still have lost because success requires more than a simple majority. See list below:

Where 100% in favour would fail

The following list assumes 100% of directed proxies went in favour of my tilt at the board but undirected proxies were voted against by the chairman in a poll. Professor Fels queried the top NRMA figure and it was explained to him that then chairman Nick Whitlam had run a very distorted election which urged shareholders to only tick three of the four boxes. He then scooped up all my blank boxes as undirected proxies which comprised 55% of the total vote and would have reduced my 100% in favour down to just 45% if there had been a poll. How can you hold directors to account for outrageous pay abuses when the corporate voting system is so flawed?

NRMA, 2000: 45.07%

WA News, 2008: 53.3%

ASX, 2000: 69.04%

WA News, 2000: 70.56%

ASX, 2001: 76.6%

CommBank, 2000: 77.43%

David Jones, 2000: 78.53%

AMP, 2000: 80.23%

ASX, 2002: 86.14%

WA News, 2007: 88.4%

PMP, 2001: 89.11%

NRMA, 2001: 90.39%

NAB, 2000: 90.82%

Southern Cross, 2001: 91%

John Fairfax, 2001: 91.76%

Woolworths, 2007: 93.95%

John Fairfax, 2005: 98.8%

Five important steps to improve the transparency of corporate voting

The Productivity Commissioners were looking for some concrete things they could do so these five items were bowled up in the supplementary submission:

# Full electronic audit trail of direct voting with no undirected proxies defaulting to chairman

# Executives can't vote on own remuneration reports (ie Westfield, Toll, Centro Retail, Gunns)

# Disclose how institutions vote and allow scrutineers as in political elections

# Church and state separation between banks and fund manager – unbundle financial conglomerates

# End effective monopoly boards have over shareholder resolutions by adopting US system where any shareholder owning $US2000 worth of stock for 12 months can put up a resolution. Australia requires 100 shareholder signatures or 5% of stock which rarely happens.

In terms of other suggestions that came out during the conversation, I supported the idea that if a company gets a protest vote of more than 10% against its remuneration report, the chairman of the rem committee should automatically face an election at the next AGM.

Similarly, when exploring the issue of which salary packages should be disclosed in the annual report, after some back and forth debate with Allan Fels, I agreed it should be all directors, the five most senior executives PLUS the next five most highly paid employees.

Risk Metrics defends power in 100 minutes before PC

Dean Paatsch and Martin Lawrence from the giant proxy adviser Risk Metrics have done more than anyone else in Australia to deliver those big 40%-plus protest votes against directors listed further up in the edition. The duo presented for 100 minutes at the PC hearings on Thursday and did actually cop some direct questions about their power, which was partly triggered by this paragraph in our supplementary submission:

Claim: proxy advisers have too much power

Yes, but on the whole they've used this power as a force for good. However, the donkey vote that Risk Metric carries is extraordinary. My average vote in 35 board tilts is 15% but the one time when Risk Metrics recommended at Centro Retail AGM last year, 70% of independent vote went my way.

Dean Paatsch batted the power question away by claiming institutions voluntarily subscribe to the service, they are not compelled to follow the advice and the firm is only as good as its last report.

Another capital raising feature for Fairfax

What started off as one story requested by my boss at Fairfax Digital has now turned into a 4-part 7000-word series about capital raisings that has attracted more than 600,000 page views.

The latest effort received more than 80,000 page views and revealed that a small Santos shareholder applied for more than $100 million in extra shares in the recent entitlement offer. No wonder Santos came up with a uniquely punitive scale back policy to punish this institution masquarading as a punter. The story also highlighted the gaming of record dates, as was seen in the Macquarie Leisure saga.

With 9 columns now contributed to Fairfax, they've put together this package of all our contributions since starting in late March.

Buying the Asciano share register

Asciano chairman Tim Poole rang last Friday afternoon and we had a 30-minute conversation, even tweeting about it half way through.

The call was triggered by this scathing attack I'd written on the Asciano capital raising for Fairfax, plus some comments when chatting with Lindy Burns during the regular spot on 774 ABC Melbourne on June 17.

Asciano was also a little taken aback when I formally requested a copy of its share register for the purposes of potentially soliciting 100 shareholders to call an EGM or put up a shareholder resolution at the next AGM.

It was a useful and cordial chat with Mr Poole, ableit off the record, and the company has now agreed to provide a copy of the register once the requisite $250 cheque has arrived at its St Kilda Rd head office.

Amusingly, Poole and I share some tennis history. As a 12 year old he was the first person to play Tasmanian and former French Open semi-finalist Richard Fromberg on the Australian mainland. I got cleaned up 8-2 an hour later in the second round of the Ringwood junior tournament at Heathmont Tennis Club in Melbourne's eastern suburbs way back in about 1982.

Urging NAB to do another SPP

The following email was sent to NAB's chairman Michael Chaney, CEO Cameron Clyne and various other relevent personnel on Monday afternoon:

Dear top NABbers,

On behalf of your retail shareholder base, I'd like to politely suggest you embark on a share purchase plan to help fund today's Aviva acquisition.

As this piece on the Fairfax websites points out, NAB's last placement/SPP capital raising had one of the lowest retail components we've seen in the recent spate of offerings at just 7.7%.

Given that Macquarie raised more from its retail investors than through its $500 million institutional placement and CBA brought in 30% of its latest capital raising from retail investors, surely now would be a good time for NAB to launch an SPP, taking advantage of the expanded maximum of $15,000.

After all, the institutions who bought $3 billion worth of your stock at $20 in that selective placement last December are tonight $373.5 million in front. The retail investors who bought $250 million worth of NAB stock at $19.97 in the follow through SPP are collectively only $31.17 million in front. Your share register is certainly not 90% institutional yet that's how the latest capital raising has divided up the profits.

Give you've stated today that you can handle the 15 point drop in tier 1 capital, why not just launch a leisurely non-underwritten SPP. Can I suggest appropriate pricing would be $22 a share or a 5% discount to VWAP up until the close.

I hope you'll look favourably at this suggestion because retail investors as a class have been diluted to the tune of billions during the recent spate of capital raisings.

As a company that looks after the savings of millions of Australians, this would send a good message that you recognise the need to accommodate small investors, not just the big end of town. Us small investors would also happily help you raise a few hundred million without gouging out an under-writing fee of 2%-plus.

Sorry for spraying you with a group email and I look forward to a reply. Better still, don't reply at all but just announce the SPP.

Best wishes, Stephen Mayne

Small NAB shareholder

Five days later, a reply from NAB

The following came back from NAB's Michaela Healey late on Friday afternoon:

Hi Stephen

Thank you for your note.

We do keep this issue under regular review as we recognise that our retail shareholders appreciate the opportunity to support the NAB via share purchase plans and a number of our retail shareholders say they are willing to support NAB in this way.

We included a retail SPP as a key component of our last capital raising. The scale of the SPP (approx $250 million) represented the level of demand rather than a limit that we had set. We were pleased that we were able to obtain regulator approval to lift the cap on SPP subscription to $10K for participation. We are now mindful that a number of our shareholders who might be interested in subscribing to a NAB SPP may not be willing to participate as they may be approaching the ASIC limit for annual SPP participation.

In offering a healthy 3% discount on our DRP for our interim dividend we have been keen to encourage shareholders to increase their shareholding without incurring any brokerage costs.

I confirm that we continue to keep this under review because we appreciate the support of our retail shareholders and we consider an SPP an effective form of capital raising.

regards, Michaela

CommQuest restructures debt, keeps on spinning

The fast-talking lads at teetering marketing services company CommQuest have finally come up with this debt restructuring that will also thankfully see 30-year-old CEO Will Scott bail out within six months.

As you might remember, CommQuest is the outfit which spent $1 million of ANZ's money on a hare-brained launch of its Bongo SMS business which included the indulgence of flying out the Hilton sisters for their New Year's Eve party in Sydney. It was a popular yarn on the Fairfax websites, generating more than 250,000 page views in one day.

The website www.smartcompany.com.au has been the PR platform of choice for Will Scott throughout the rise and fall of Commquest and he's been at it again with this interview spruiking the debt restructure.

And speaking of Smart Company, they've published a big Q&A interview with your correspondent this week which runs over three pages. As you'll see, there's a great deal of pessimism about the future of well paid online and newspaper journalism.

City Pacific given the boot - hooray

History was made yesterday when City Pacific was dumped as the manager of its troubled $1 billion mortgage fund due to atrocious performance and ridiculous fee-gouging. Sucked in to the Commonwealth Bank for potentially having to take a write-off on its $100 million-plus City Pacific exposure now that those out-rageous fees won't be gouged any more.

Cornwall: Turnbull now a big asset for Rudd Government

More active than ever

As you can see from this list of all our recent trades, we've never been more active than ever in June. The individual capital raising plays are fully listed online and in monthly terms the gross profits have been as follows:

January: $400 loss

February: $120 loss

March: $10,170 profit

April: $36,996 profit

May: $23,639 profit

June: $75,000 profit so far

The gross figure is a bit misleading because there has been almost $20,000 in underwriting and financing costs associated with all these plays and we're now only back to break even overall courtesy of all the earlier losses from the market crunch.

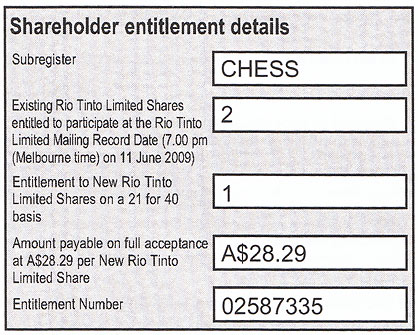

A tiny offer from Rio

When you're a tiny shareholder in everything, pro-rata capital raisings shouldn't produce big money making opportunities. And so it is with Rio Tinto which is not allowing shareholders to apply for any more shares than their entitlement. In my case, it's pretty small:

GPT offer and cheque

Speaking of refund cheques and small allocations, check out what came back from GPT.

Saving Ventracor

Ventracor is one of those promising Aussie health tech plays that is now "under administration" with Steve Sherman of Ferrier Hodgson. Quite a few shareholders reckons it shouldn't be sold off to American investors, but instead retained and refashioned into the next Resmed or Cochlear.

Check out some of their efforts on the website: www.saveventracor.com.

The small committee of shareholders are fighting a losing battle and need an Aussie financier for about $10 million to inject into the company to go on and finish the Heart Pump Device which is proving satisfactory in trials, and is near fruition to start production in about 12 months time.

They raised about $50,000 as a fighting fund but need some more exposure to attract the bigger dollars needed.

Press room and latest radio interviews

The best way to listen to our regular radio interviews is to sign up for video and audio podcasts. The past week has included additions to this major series on capital raisings for Fairfax websites.

Profiting at Leisure

There's still time to make some money off Macquarie Leisure - but you have to move today.

June 29, 2009

Easy money on the table

The odds are stacked against small investors as companies rush to raise billions. Here's how to get a fairer roll of the dice.

June 23, 2009

How small investors miss out

Ripping into MacMahon, Asciano and the whole dodgy system of placements and scale backs.

June 16, 2009

June 17, 774 ABC Melbourne - regular chat with Lindy Burns

June 24, 774 ABC Melbourne - regular chat with Lindy Burns

Also, check out these special packages for our other regular media spots. We've spent plenty of time re-arranging the press room so check it out here.

Child of Tibet - a lost innocence

The Mayne Report's multimedia guy Shane Marden has self-published this delightful photography book about the beauty of Tibet and its people. The Dalai Lama has written a foreword for the book and from sales Shane has decided to donate funds to the Australian Tibet Council. It has taken a few years for Shane to publish the book, but the result is a beautiful, heartfelt publication. There are 1800 copies for sale as a first edition and I encourage all of you to visit his site to purchase a copy online, or to see a list of bookstores where the book is available.

Traffic on the rise

The Mayne Report is becoming more popular every month. The two most popular pages have been our 2009 share activity, and our video blog page with 11,000 views each. If you haven't visited yet, here you can view the best videos we have made over the past two years, and also collections of special edition videos. If you are always on the move, sign up for our podcasts so you can hear our radio grabs, AGM appearances and watch the videos on your ipod, whilst sitting on the train.

Tweet us on Twitter

We only joined Twitter around a month ago, but we have collected more than 300 followers thus far. Recently we have witnessed the connectivity success of Twitter in Iran, and the power of information transfer. We encourage you to join our tweet stream to see up to the minute what we are up to.

Cornwall cartoons for The Mayne Report

Former Fairfax and Crikey cartoonist Mark Cornwall has been contributing his satirical commentary to the Mayne Report since March 2009. Here is a collection of his best cartoons and there are now some amusing animations he has begun. Go here to see his animation and below are some new offerings:

Mayne Report video blog

Over the past few weeks we have been putting together playlists of videos covering similar topics and additionally, collections of videos from television appearances. Check out these special edition videos.

The Mayne Report Rich List

Since we began compiling the Mayne Report Rich List documenting every Australian currently or previously worth more then $10 million, it has grown in numbers and popularity such that no other feature on our website can match it for traffic.

We're now up to 1370 entries, although some are italicised, denoting that they are no longer worth more than our $10 million cut off. Here are our latest entries, some of which have come courtesy of the latest edition of BRW's execellent Rich List:

Chris Clarke: based in the US and a former advertising industry guru, he founded and sold his Australian advertising agency, Pure Creative in 2000. He then began a global advertising agency called Nitro which was bought out by Sapient, and from this sale he pocketed a handy $US42.5 million.

Scott Hosking: a former scrap-metal trader and founding director of Nexus Energy, he is also the chief financial officer and company secretary of Karoon Gas. He has a stake worth more than $80 million largely due to a large gas deposit discovered at the Poseidon well which is one of the biggest discoveries by a small Australian explorer.

All the recent share trades

We've continued with all this tax-loss selling of late after this run of wins from capital raisings. Check out all the trades so far this year. Below is the state of play over the past few months, with spreadsheets available if you click on the dates. The losses have come down recently because we've been doing plenty of tax-loss selling after some windfall gains playing the angles on capital raisings, as was explained in this piece for the Fairfax websites.

June 18, 2009: portfolio of 698 stocks worth $194,716 with paper loss of $3,298. Average holding $279.

June 25

AMP: sold 90 at $4.85

Macquarie Leisure: bought 335 at $1.505

Photon Group: sold 300 at $1.62

Qantas: sold 210 at $2.02

Transfield Services Infrastructure fund: sold 465 at 99c

Valad Property Group: sold 6500 at 7.2c

June 24

Stockland: sold 5,000 at $2.81

June 23

Asian Masters Fund: bought 500 at $1.05

BC Iron: sold 385 at $1.10

Kagara: sold 429 at 65c

Stockland: sold 7407 at $3.01

June 22

Aura Energy: bought 3850 at 13c

Billabong: bought 4000 at $7.50 in entitlement offer

Billabong: sold 4000 at $8.20

Cluff Resources Pacific: bought

Kairiki Energy: bought 2780 at 18c

National Australia Bank: bought 25 at $22.26

Saracen Mineral Holdings: bought 2440 at 20.5c

Swick Mining Services: bought 1112 at 45c

June 19

AMP: bought 100 at $5.10

BC Iron: bought $3.95

BC Iron: bought 390 at $1.29

Central Petroleum: bought 5000 at 10.5c

Cougar Energy: sold 4300 at 11.5c

Macarthur Coal: bought 80 at $6.30

Roc Oil: sold 680 at 86.5c

Stockland: sold 3000 at $3.01

Tower Australia: bought 187 at $2.70

Tower Australia: bought 190 at $2.67

Valad Property Group: bought 6600 at 7.7c

June 18

Stockland: bought 31,000 in entitlement offer at $2.70

Stockland: sold 3000 at $3.07

Transfield Services Infrastructure Fund: bought 475 at $1.06

June 17

Bluescope Steel: sold 3000 at $2.51

Santos: bought 2675 at $12.50 in entitlement offer

Santos: sold 2675 at $14.10

Seek: bought 1030 at $2.60 in SPP

Seek: sold 1030 at $4.11

Finally, if you've missed some of our earlier member editions, check them all out here.

That's all for now, thanks for getting to the bottom and do send through some feedback to stephen@maynereport.com.

We'll be back in touch next week.

Do ya best, Stephen Mayne

* If you're reading this without being on our email list, why not sign up for free and tell your friends as well. Alternatively, if you've had enough, click here to unsubscribe.

Macquarie dunderheads leave the door open

Crikey founder Stephen Mayne writes:

Want to make a leisurely $5000 in a few weeks? Buy $500 worth of shares in Macquarie Leisure (ASX code: MLE) before close of trade on Monday and you're in with a shot.

The Millionaires Factory and the Macquarie Leisure board have shown themselves to be complete dills in the way they've structured the management internalisation and capital raising announced yesterday.

First up, they've done a highly dilutive $41.7 million share placement at only $1.15 each. Surely the board knew that the shares would be re-rated once the $3-5 million fee leakage to Macquarie each year had been eliminated.

Sure enough Macquarie Leisure shares jumped 15c to $1.50 when trade resumed this morning and the board announced that the selective placement to the big end of town was “significantly over-subscribed”.

No wonder, these lucky clients of under-writers Macquarie and RBS have made a paper profit of more than $10 million. Where was the price tension? Where was the book build to minimise dilution?

The existing Macquarie Leisure shareholders will be further diluted because the dunderheads have announced a $15,000 share purchase plan for retail investors with a record date of next Thursday, July 2.

Therefore, anyone who buys $500 worth of shares before close of trading on Monday will qualify to apply for $15,000 worth of shares in the SPP at only $1.15 a pop.

I was already on the register but the wife, another relative and an employee have each bought another $500 worth this morning meaning we'll be collectively stumping up $60,000 in an attempt to make a quick $20,000 profit.

However, as was explained in this piece for the Fairfax websites on June 23, the only problem is that thousands of other opportunists and day traders will jump on the arbitrage, especially now that the secret is being shared with the vast Crikey army. (Well, actually no, they declined to run the story!)

It's money for jam and this is what one UBS adviser sent to all his clients today:

We have become aware of a small arbitrage opportunity in MLE which are currently in the process of issuing shares as part of a share purchase plan (capital raising). Shareholders have the right to purchase up to $15,000 worth of shares at $1.15 which equates to approximately 13,000 units. Providing the share price holds (currently $1.50) for the period of the offer, this represents a profit of $5,000 or 30.0% on an investment of $15,000.

Macquarie Leisure has said there is only $18.3 million available for the SPP, so it is likely to be massively over-subscribed and heavily scaled back.

Macquarie Leisure CEO Greg Shaw said the company only had 7000 retail shareholders and adding a few more in the next two trading days would boost liquidity and turnover which in turn could help the stock make the ASX200.

Whilst Shaw admitted that “obviously this is an opportunity for some people to take up”, he claimed the board “was not actively encouraging it”.

Yeah, but we are Greg and with the ability to spread news fast online, you are going to see thousands of new Macquarie Leisure shareholders buy before Monday's deadline.

Assuming Macquarie Leisure finishes with 10,000 eligible shareholder on board by next Thursday's record date, that's a potential $150 million worth of applications chasing $18.3 million, so the scale back will probably be huge.

Finally, check out this list of other companies which have left the gate open for opportunists during the record breaking run of heavily discounted capital raisings.

It just shouldn't happen and who would have thought the Millionaires Factory would join the club. Indeed, it would be interesting to know if Macquarie Bank employees are allowed to join in the party, all of which is being funded by the existing Macquarie Leisure shareholders who suffer completely unnecessary dilution.

Some bouquets for Macquarie Leisure directors

Leaving aside all those brickbats on what is ultimately a fairly immaterial issue in financial terms, the non-executive directors of Macquarie Leisure, led by Anne Keating and chairman Neil Balnaves, are to be congratulated for successfully breaking free of the Millionaires Factory.

Macquarie obviously drove a hard bargain extracting $17 million for its management contract, but I understand the whole process was actually driven by the independent directors who took their responsibilities seriously. Macquarie didn't seek or particularly want the deal and negotiated in their usual aggressive way.

Anyone who thinks this automatically means Macquarie Airports and Macquarie Infrastructure Group will go the same way ought to look at just who are the independent directors on those boards.

MAP in particular is stacked with Macquarie partisans and Bermudan box tickers, whilst MIG features Leighton chairman David Mortimer, who used to have his office at Macquarie. If only MIG and MAP followed the Macquarie Leisure by having an independent chairman, rather than Mark Johnson and Max Moore-Wilton respectively.

The best thing about Macquarie Leisure's internalisation proposal is that CEO Greg Shaw will now actually work for the directors and the shareholders, rather than being employed by Macquarie on a salary that has never been disclosed.

Fronting Felsy and friends at the PC pay inquiry

Canberra fog delayed the start of the Melbourne hearings of the Productivity Commission's executive pay inquiry so a one hour appearance for your correspondent scheduled to commence at 9.30am on Wednesday turned into a lively 70-minute exchange starting at 12.10pm.

The three commissioners had only been furnished with this original two-page submission so the delay provided the extra two hours necessary to come up with another two pages to present on the day. Some of that material is reproduced below. The key message was that we need to fix the system of director elections in Australia and to demonstrate the problem the following was produced:

Biggest remuneration report protest - why back the directors?

This list tracks the 13 protest votes exceeding 40% against remunerations reports at ASX200 companies since 2006 and shows how the unidentified institutional shareholders backed the directors at the same AGMs who got the pay policies wrong. If you vote against remuneration reports, surely you should vote against the responsible directors.

Valad Property Group, 2008: 76.1% against rem - big bonuses as company close to collapse.

Least popular director: Bob Seidler, 85.8% in favour

Telstra, 2007: 66.18% against rem - not enough performance hurdles or disclosure for Sol Trujillo.

No directors up for election.

AGL, 2007: 62.56% against rem – CEO Paul Anthony pocketed $17 million for 17 months work.

Least popular director: chairman Mark Johnson: 83.2% in favour

Transurban, 2008: 58.56% against rem - $16.6 million farewell to former CEO Kim Edwards.

Least popular director: chairman David Ryan, only 57.1% in favour due to ABC Learning baggage.

Boral, 2008: 58% against rem - big increase in base pay and short term bonuses for CEO Rod Pearce.

Least popular director: Paul Rayner, 99.5% in favour

Wesfarmers, 2008: 50.50% against rem - poor disclosure of incentive scheme for CEO Richard Goyder.

Least popular director: chairman Bob Every, 99.5% in favour

Oxiana, 2006: 46.9% against rem - changed the performance period on CEO Owen Hegarty's options.

Least popular director: Michael Eager, 99.3% in favour

Alumina, 2007: 46.2% against rem - CEO incentives not structured appropriately.

Least popular director: Peter Hay, 99.2% in favour

MFS, 2007: 45.92% against rem - options for chair Andrew Peacock and excessive cash for executives.

Least popular director: Paul Manka, 99.2% in favour

Toll Holdings, 2008: 42.94% against rem - big protest against $55m options buyout in Asciano demerger.

Least popular director: chairman Ray Horsburgh: 99.7% in favour

Qantas, 2008, 41.48% against rem – Geoff Dixon highest paid airline CEO in the world.

Least popular director: Barbara Ward: 59% in favour

Zinifex, 2006: 41.26% against rem - excessive $12 million incentive payment to outgoing CEO Greg Gailey.

Least popular director: Tony Larkin, 99.9% in favour

Suncorp, 2007: 40.61% against rem - excessive incentive payments guaranteed after Promina takeover.

Least popular director: Dr Cherrell Hirst, 98% in favour.

Fix corporate voting, especially the no vacancy rort

The key to corporate governance, including executive pay, is fixing up the director election system. The biggest problem is where boards require a challenger to knock off an incumbent to get elected by declaring there is “no vacancy”. The average incumbent gets 96% in favour and when you throw in the typical 10% of the vote as undirected proxies in the chairman's back pocket, it was statistically impossible for me to get elected in the majority of 35 board tilts. 100% of directed proxies in favour would still have lost because success requires more than a simple majority. See list below:

Where 100% in favour would fail

The following list assumes 100% of directed proxies went in favour of my tilt at the board but undirected proxies were voted against by the chairman in a poll. Professor Fels queried the top NRMA figure and it was explained to him that then chairman Nick Whitlam had run a very distorted election which urged shareholders to only tick three of the four boxes. He then scooped up all my blank boxes as undirected proxies which comprised 55% of the total vote and would have reduced my 100% in favour down to just 45% if there had been a poll. How can you hold directors to account for outrageous pay abuses when the corporate voting system is so flawed?

NRMA, 2000: 45.07%

WA News, 2008: 53.3%

ASX, 2000: 69.04%

WA News, 2000: 70.56%

ASX, 2001: 76.6%

CommBank, 2000: 77.43%

David Jones, 2000: 78.53%

AMP, 2000: 80.23%

ASX, 2002: 86.14%

WA News, 2007: 88.4%

PMP, 2001: 89.11%

NRMA, 2001: 90.39%

NAB, 2000: 90.82%

Southern Cross, 2001: 91%

John Fairfax, 2001: 91.76%

Woolworths, 2007: 93.95%

John Fairfax, 2005: 98.8%

Five important steps to improve the transparency of corporate voting

The Productivity Commissioners were looking for some concrete things they could do so these five items were bowled up in the supplementary submission:

# Full electronic audit trail of direct voting with no undirected proxies defaulting to chairman

# Executives can't vote on own remuneration reports (ie Westfield, Toll, Centro Retail, Gunns)

# Disclose how institutions vote and allow scrutineers as in political elections

# Church and state separation between banks and fund manager – unbundle financial conglomerates

# End effective monopoly boards have over shareholder resolutions by adopting US system where any shareholder owning $US2000 worth of stock for 12 months can put up a resolution. Australia requires 100 shareholder signatures or 5% of stock which rarely happens.

In terms of other suggestions that came out during the conversation, I supported the idea that if a company gets a protest vote of more than 10% against its remuneration report, the chairman of the rem committee should automatically face an election at the next AGM.

Similarly, when exploring the issue of which salary packages should be disclosed in the annual report, after some back and forth debate with Allan Fels, I agreed it should be all directors, the five most senior executives PLUS the next five most highly paid employees.

Risk Metrics defends power in 100 minutes before PC

Dean Paatsch and Martin Lawrence from the giant proxy adviser Risk Metrics have done more than anyone else in Australia to deliver those big 40%-plus protest votes against directors listed further up in the edition. The duo presented for 100 minutes at the PC hearings on Thursday and did actually cop some direct questions about their power, which was partly triggered by this paragraph in our supplementary submission:

Claim: proxy advisers have too much power

Yes, but on the whole they've used this power as a force for good. However, the donkey vote that Risk Metric carries is extraordinary. My average vote in 35 board tilts is 15% but the one time when Risk Metrics recommended at Centro Retail AGM last year, 70% of independent vote went my way.

Dean Paatsch batted the power question away by claiming institutions voluntarily subscribe to the service, they are not compelled to follow the advice and the firm is only as good as its last report.

Another capital raising feature for Fairfax

What started off as one story requested by my boss at Fairfax Digital has now turned into a 4-part 7000-word series about capital raisings that has attracted more than 600,000 page views.

The latest effort received more than 80,000 page views and revealed that a small Santos shareholder applied for more than $100 million in extra shares in the recent entitlement offer. No wonder Santos came up with a uniquely punitive scale back policy to punish this institution masquarading as a punter. The story also highlighted the gaming of record dates, as was seen in the Macquarie Leisure saga.

With 9 columns now contributed to Fairfax, they've put together this package of all our contributions since starting in late March.

Buying the Asciano share register

Asciano chairman Tim Poole rang last Friday afternoon and we had a 30-minute conversation, even tweeting about it half way through.

The call was triggered by this scathing attack I'd written on the Asciano capital raising for Fairfax, plus some comments when chatting with Lindy Burns during the regular spot on 774 ABC Melbourne on June 17.

Asciano was also a little taken aback when I formally requested a copy of its share register for the purposes of potentially soliciting 100 shareholders to call an EGM or put up a shareholder resolution at the next AGM.

It was a useful and cordial chat with Mr Poole, ableit off the record, and the company has now agreed to provide a copy of the register once the requisite $250 cheque has arrived at its St Kilda Rd head office.

Amusingly, Poole and I share some tennis history. As a 12 year old he was the first person to play Tasmanian and former French Open semi-finalist Richard Fromberg on the Australian mainland. I got cleaned up 8-2 an hour later in the second round of the Ringwood junior tournament at Heathmont Tennis Club in Melbourne's eastern suburbs way back in about 1982.

Urging NAB to do another SPP

The following email was sent to NAB's chairman Michael Chaney, CEO Cameron Clyne and various other relevent personnel on Monday afternoon:

Dear top NABbers,

On behalf of your retail shareholder base, I'd like to politely suggest you embark on a share purchase plan to help fund today's Aviva acquisition.

As this piece on the Fairfax websites points out, NAB's last placement/SPP capital raising had one of the lowest retail components we've seen in the recent spate of offerings at just 7.7%.

Given that Macquarie raised more from its retail investors than through its $500 million institutional placement and CBA brought in 30% of its latest capital raising from retail investors, surely now would be a good time for NAB to launch an SPP, taking advantage of the expanded maximum of $15,000.

After all, the institutions who bought $3 billion worth of your stock at $20 in that selective placement last December are tonight $373.5 million in front. The retail investors who bought $250 million worth of NAB stock at $19.97 in the follow through SPP are collectively only $31.17 million in front. Your share register is certainly not 90% institutional yet that's how the latest capital raising has divided up the profits.

Give you've stated today that you can handle the 15 point drop in tier 1 capital, why not just launch a leisurely non-underwritten SPP. Can I suggest appropriate pricing would be $22 a share or a 5% discount to VWAP up until the close.

I hope you'll look favourably at this suggestion because retail investors as a class have been diluted to the tune of billions during the recent spate of capital raisings.

As a company that looks after the savings of millions of Australians, this would send a good message that you recognise the need to accommodate small investors, not just the big end of town. Us small investors would also happily help you raise a few hundred million without gouging out an under-writing fee of 2%-plus.

Sorry for spraying you with a group email and I look forward to a reply. Better still, don't reply at all but just announce the SPP.

Best wishes, Stephen Mayne

Small NAB shareholder

Five days later, a reply from NAB

The following came back from NAB's Michaela Healey late on Friday afternoon:

Hi Stephen

Thank you for your note.

We do keep this issue under regular review as we recognise that our retail shareholders appreciate the opportunity to support the NAB via share purchase plans and a number of our retail shareholders say they are willing to support NAB in this way.

We included a retail SPP as a key component of our last capital raising. The scale of the SPP (approx $250 million) represented the level of demand rather than a limit that we had set. We were pleased that we were able to obtain regulator approval to lift the cap on SPP subscription to $10K for participation. We are now mindful that a number of our shareholders who might be interested in subscribing to a NAB SPP may not be willing to participate as they may be approaching the ASIC limit for annual SPP participation.

In offering a healthy 3% discount on our DRP for our interim dividend we have been keen to encourage shareholders to increase their shareholding without incurring any brokerage costs.

I confirm that we continue to keep this under review because we appreciate the support of our retail shareholders and we consider an SPP an effective form of capital raising.

regards, Michaela

CommQuest restructures debt, keeps on spinning

The fast-talking lads at teetering marketing services company CommQuest have finally come up with this debt restructuring that will also thankfully see 30-year-old CEO Will Scott bail out within six months.

As you might remember, CommQuest is the outfit which spent $1 million of ANZ's money on a hare-brained launch of its Bongo SMS business which included the indulgence of flying out the Hilton sisters for their New Year's Eve party in Sydney. It was a popular yarn on the Fairfax websites, generating more than 250,000 page views in one day.

The website www.smartcompany.com.au has been the PR platform of choice for Will Scott throughout the rise and fall of Commquest and he's been at it again with this interview spruiking the debt restructure.

And speaking of Smart Company, they've published a big Q&A interview with your correspondent this week which runs over three pages. As you'll see, there's a great deal of pessimism about the future of well paid online and newspaper journalism.

City Pacific given the boot - hooray

History was made yesterday when City Pacific was dumped as the manager of its troubled $1 billion mortgage fund due to atrocious performance and ridiculous fee-gouging. Sucked in to the Commonwealth Bank for potentially having to take a write-off on its $100 million-plus City Pacific exposure now that those out-rageous fees won't be gouged any more.

Cornwall: Turnbull now a big asset for Rudd Government

More active than ever

As you can see from this list of all our recent trades, we've never been more active than ever in June. The individual capital raising plays are fully listed online and in monthly terms the gross profits have been as follows:

January: $400 loss

February: $120 loss

March: $10,170 profit

April: $36,996 profit

May: $23,639 profit

June: $75,000 profit so far

The gross figure is a bit misleading because there has been almost $20,000 in underwriting and financing costs associated with all these plays and we're now only back to break even overall courtesy of all the earlier losses from the market crunch.

A tiny offer from Rio

When you're a tiny shareholder in everything, pro-rata capital raisings shouldn't produce big money making opportunities. And so it is with Rio Tinto which is not allowing shareholders to apply for any more shares than their entitlement. In my case, it's pretty small:

GPT offer and cheque

Speaking of refund cheques and small allocations, check out what came back from GPT.

Saving Ventracor

Ventracor is one of those promising Aussie health tech plays that is now "under administration" with Steve Sherman of Ferrier Hodgson. Quite a few shareholders reckons it shouldn't be sold off to American investors, but instead retained and refashioned into the next Resmed or Cochlear.

Check out some of their efforts on the website: www.saveventracor.com.

The small committee of shareholders are fighting a losing battle and need an Aussie financier for about $10 million to inject into the company to go on and finish the Heart Pump Device which is proving satisfactory in trials, and is near fruition to start production in about 12 months time.

They raised about $50,000 as a fighting fund but need some more exposure to attract the bigger dollars needed.

Press room and latest radio interviews

The best way to listen to our regular radio interviews is to sign up for video and audio podcasts. The past week has included additions to this major series on capital raisings for Fairfax websites.

Profiting at Leisure

There's still time to make some money off Macquarie Leisure - but you have to move today.

June 29, 2009

Easy money on the table

The odds are stacked against small investors as companies rush to raise billions. Here's how to get a fairer roll of the dice.

June 23, 2009

How small investors miss out

Ripping into MacMahon, Asciano and the whole dodgy system of placements and scale backs.

June 16, 2009

June 17, 774 ABC Melbourne - regular chat with Lindy Burns

June 24, 774 ABC Melbourne - regular chat with Lindy Burns

Also, check out these special packages for our other regular media spots. We've spent plenty of time re-arranging the press room so check it out here.

Child of Tibet - a lost innocence

The Mayne Report's multimedia guy Shane Marden has self-published this delightful photography book about the beauty of Tibet and its people. The Dalai Lama has written a foreword for the book and from sales Shane has decided to donate funds to the Australian Tibet Council. It has taken a few years for Shane to publish the book, but the result is a beautiful, heartfelt publication. There are 1800 copies for sale as a first edition and I encourage all of you to visit his site to purchase a copy online, or to see a list of bookstores where the book is available.

Traffic on the rise

The Mayne Report is becoming more popular every month. The two most popular pages have been our 2009 share activity, and our video blog page with 11,000 views each. If you haven't visited yet, here you can view the best videos we have made over the past two years, and also collections of special edition videos. If you are always on the move, sign up for our podcasts so you can hear our radio grabs, AGM appearances and watch the videos on your ipod, whilst sitting on the train.

Tweet us on Twitter

We only joined Twitter around a month ago, but we have collected more than 300 followers thus far. Recently we have witnessed the connectivity success of Twitter in Iran, and the power of information transfer. We encourage you to join our tweet stream to see up to the minute what we are up to.

Cornwall cartoons for The Mayne Report

Former Fairfax and Crikey cartoonist Mark Cornwall has been contributing his satirical commentary to the Mayne Report since March 2009. Here is a collection of his best cartoons and there are now some amusing animations he has begun. Go here to see his animation and below are some new offerings:

Mayne Report video blog

Over the past few weeks we have been putting together playlists of videos covering similar topics and additionally, collections of videos from television appearances. Check out these special edition videos.

The Mayne Report Rich List

Since we began compiling the Mayne Report Rich List documenting every Australian currently or previously worth more then $10 million, it has grown in numbers and popularity such that no other feature on our website can match it for traffic.

We're now up to 1370 entries, although some are italicised, denoting that they are no longer worth more than our $10 million cut off. Here are our latest entries, some of which have come courtesy of the latest edition of BRW's execellent Rich List:

Chris Clarke: based in the US and a former advertising industry guru, he founded and sold his Australian advertising agency, Pure Creative in 2000. He then began a global advertising agency called Nitro which was bought out by Sapient, and from this sale he pocketed a handy $US42.5 million.

Scott Hosking: a former scrap-metal trader and founding director of Nexus Energy, he is also the chief financial officer and company secretary of Karoon Gas. He has a stake worth more than $80 million largely due to a large gas deposit discovered at the Poseidon well which is one of the biggest discoveries by a small Australian explorer.

All the recent share trades

We've continued with all this tax-loss selling of late after this run of wins from capital raisings. Check out all the trades so far this year. Below is the state of play over the past few months, with spreadsheets available if you click on the dates. The losses have come down recently because we've been doing plenty of tax-loss selling after some windfall gains playing the angles on capital raisings, as was explained in this piece for the Fairfax websites.

June 18, 2009: portfolio of 698 stocks worth $194,716 with paper loss of $3,298. Average holding $279.

June 25

AMP: sold 90 at $4.85

Macquarie Leisure: bought 335 at $1.505

Photon Group: sold 300 at $1.62

Qantas: sold 210 at $2.02

Transfield Services Infrastructure fund: sold 465 at 99c

Valad Property Group: sold 6500 at 7.2c

June 24

Stockland: sold 5,000 at $2.81

June 23

Asian Masters Fund: bought 500 at $1.05

BC Iron: sold 385 at $1.10

Kagara: sold 429 at 65c

Stockland: sold 7407 at $3.01

June 22

Aura Energy: bought 3850 at 13c

Billabong: bought 4000 at $7.50 in entitlement offer

Billabong: sold 4000 at $8.20

Cluff Resources Pacific: bought

Kairiki Energy: bought 2780 at 18c

National Australia Bank: bought 25 at $22.26

Saracen Mineral Holdings: bought 2440 at 20.5c

Swick Mining Services: bought 1112 at 45c

June 19

AMP: bought 100 at $5.10

BC Iron: bought $3.95

BC Iron: bought 390 at $1.29

Central Petroleum: bought 5000 at 10.5c

Cougar Energy: sold 4300 at 11.5c

Macarthur Coal: bought 80 at $6.30

Roc Oil: sold 680 at 86.5c

Stockland: sold 3000 at $3.01

Tower Australia: bought 187 at $2.70

Tower Australia: bought 190 at $2.67

Valad Property Group: bought 6600 at 7.7c

June 18

Stockland: bought 31,000 in entitlement offer at $2.70

Stockland: sold 3000 at $3.07

Transfield Services Infrastructure Fund: bought 475 at $1.06

June 17

Bluescope Steel: sold 3000 at $2.51

Santos: bought 2675 at $12.50 in entitlement offer

Santos: sold 2675 at $14.10

Seek: bought 1030 at $2.60 in SPP

Seek: sold 1030 at $4.11

Finally, if you've missed some of our earlier member editions, check them all out here.

That's all for now, thanks for getting to the bottom and do send through some feedback to stephen@maynereport.com.

We'll be back in touch next week.

Do ya best, Stephen Mayne

* If you're reading this without being on our email list, why not sign up for free and tell your friends as well. Alternatively, if you've had enough, click here to unsubscribe.