Elders rip-off, NAB excuses, Woolies grog push, Virgin scale back, Australand windfall, McCrann, Walkleys, activism, Macek, AMP and much more

February 2, 2010

Dear Mayne Reporters,

apologies it was 11 days between editions but we hope you'll think it was worth the wait.

Staggering 52 companies join $100 million loss club

When a record 29 ASX-listed companies reported losses of more than $100 million in 2007-08, we thought it was pretty remarkable. Amazingly, the 2008-09 season delivered unprecedented amounts of red ink, caused by the global financial crisis, with losses of more than $100 million for a record 52 companies. That's a pretty amazing statistic given that we had previously only found 75 companies that had achieved this unfortunate milestone more than 150 times over the past 20 years.

Check out where these latest losses sit in the all-time list tracking $100 million losses from biggest to smallest.

It has been a very interesting process tracking the timing of earnings results. For instance, check out this list to see when the 52 $100m-plus losses were announced. Surprise, surprise they were heavily weighted towards the last few days of the reporting season.

We gave the issue a big burst on the Fairfax websites last Friday just ahead of Elders releasing their season-ending $414 million net loss.

And check out this amazing chronological list of how 285 companies dropped their results on the last possible day.

Elders shaft big retail investors like never before

The $550 million emergency Elders capital raising has been generating plenty of press and the company comes in at number 37 on our new mega-list tracking all major capital raisings since the beginning of 2008.

The monster placement of new shares at a miserable 15c a pop surpasses even the Asciano record for retail dilution. At least with Asciano retail investors had a 1-for-1 entitlement offer and were able to apply for 2.1 times their entitlement, followed by a $10,000 share purchase plan, albeit scaled back by 65% in the end.

Asciano started the process with 700 million shares on issue and then did a placement of 2.137 billion shares - more than three times the existing capital base when the law limits companies to issuing just 15% of shares by way of placement in any 12 month period without shareholder approval.

Elders shares last traded at 39c before the capital raising and with 818 million shares on issue this capitalised the business at $319 million.

However, after all this talk of a straightforward 25c renounceable rights issue, the company came back with a whopping $400 million institutional placement that comprised issuing 2.667 billion new shares at 15c - equivalent to 3.26 times the original number of shares. Whilst there is no pro-rata entitlement offer at all, the sop to retail investors is a $150 million share purchase plan with each Australian and New Zealand investor entitled to buy up 133,333 shares at 15c each for a total of $20,000, a figure we've never seen before with an SPP.

Whilst our family are likely to be big winners from all this, the following email exchange with a sophisticated retail investor, who we'll call Warren, sums up the key problems and themes:

Warren to Mayne Report

Hi Stephen,

Disgraceful and unashamed dilution of the larger retail holders at Elders, but great for small holders like yourself assuming you get the full $20,000. What's wrong with a fully renounceable rights issue? They had some momentum but chose to give all the upside to the instos.

Will be an interesting one to dissect.

All the best, Warren

Mayne Report to Warren

I agree, amazing windfall for tiny holders, huge shafting of bigger holders. It seems refusal of biggest shareholder to participate, some UK insto with 15%, led to decision to shaft them big time.

The wife and I are both in there so windfall on tonight's close is $25,000 although the maximum uptake assuming all 32,000 shareholders participate is $640 million so likely to be scale back which they would have to skew in favour of larger retail.

My tip would be something like everyone with more than 10,000 shares gets full allocation, the rest get scaled back with a minimum allocation of perhaps $5000 to the smallest such as myself.

Anyway, time will tell but I'll write this up during the week.

Cheers, Stephen

Warren to Mayne Report

I'm OK I only hold the hybrids, which is a mixed blessing, on the one hand the risk of losing the lot is now minimal but they have suspended the dividend for 2 years and scotched the dividend on the ordinary shares for almost 3 years as collateral damage.

For the life of me I can't understand why they suspended the hybrid dividends, why would they offer it up to the debt holders? I obviously don't understand fully the re-financing but from what I can see nobody holding their debt took a haircut. As long they keep making their interest payments and stay within their covenants what comfort would not paying the hybrids give the debt holders?

Anyway the EGM will be pretty colourful, I half expect some disgruntled cockies who have held long term to turn up on horseback dressed as Ned Kelly.

Good luck to you and Paula

Mayne Report to Warren

What's the coupon on the hybrid? There's 1.5 million outstanding at $100 presumably so what's it going to save them?

Also, is it repayment at par in 2011? If so, that would be a screaming buy once shareholders approve placement/SPP given reduction in risk.

Hybrids were a big factor in collapse of Babcock & Brown and will be a major factor in recapitalisation proposal for Babcock & Brown Infrastructure. Save from putting the company under, it seems the worst they can do is suspend coupons until maturity.

Cheers, Stephen

Warren to Mayne Report

Coupon is currently bank bill swap rate plus 2.2% and will step up another 2.5% in 2011.

So I guess it is currently about $7–8m per annum, not going to drive them to the wall but not insubstantial. I guess I don't understand why they would say 2 years. The payment of the hybrid dividend is at the discretion of the directors, why limit themselves with this kind condition, if the business is going gang busters in 12 months what then? Surely would be more prudent to consider as a quarter to quarter proposition (which I reckon was the original intent of the issue). As I said if they are getting paid and the business is trading within the covenants why would the other debt holders care?

Unfortunately the hybrids are perpetual – the thinking is that 4.7% over BBSW (after step up) would probably incent the company to redeem. I guess a cynic might question this in the light of the current suspension of dividends.

Given that they have cleared the decks in terms of debt and non-core businesses the more likely trigger for redemption is a takeover. With the new look balance sheet I reckon they will be in play in the next 12 months? Dare I use the term LBO?

The trip to Adelaide for the Elders EGM on October 15 would ordinarily be a no brainer, but unfortunately it clashes with a speaking commitment at a big capital raising conference in Sydney, so if anyone fancies being the proxy, drop us a line to stephen@maynereport.com.

Contested election for NAB chairman Michael Chaney

The National Australia Bank SPP scale back scandal is starting to get a bit more mainstream media traction. Michael Pascoe powerfully called for NAB chairman Michael Chaney to be booted off the board in his end of week video for Fairfax two Friday's back and 4BC Drive presenter Mike Smith was happy to stick the boot in during this interview with your correspondent on the same day.

NAB has clearly been inundated by complaints from irate shareholders based on this letter its chairman sent out with the refund and allotment notices last week. Chaney opened up with the following:

Dear Shareholder, there has been a great deal of discussion and comment in recent days on institutional share placements and Share

Purchase Plans.

Well, not really. The AFR's letters pages have carried some debate but the top business columnists have largely been missing in action. The whole point of rushing out this edition of The Mayne Report on August 25 was to alert the mainstream media to the scandal, but it literally generated only a couple of paragraphs in The AFR on August 26.

It's not often more than 150,000 Australians get collectively shafted out of $300 million but that's what NAB did and these retail investors are clearly fuming.

The Chaney letter did trigger a page lead in The AFR last Thursday, but it contained an error so the following letter was fired off by your correspondent which was finally published in yesterday's paper as follows:

NAB's miserable 202 shares from SPP

Matthew Drummond's story (“Chaney tries to soothe NAB shareholders”, September 3) about National Australia Bank's share purchase plan claims “the maximum allotment will be $15,000”.

If only it were so. The problem with NAB is that it has slashed more than 150,000 shareholders who applied for the full $15,000 allotment down to a miserable 202 shares costing $4343.

Investors are rightly up in arms about this 71% scale back. They didn't want to collectively receive $1.85 billion in refunds, especially when no other Australian bank has ever scaled back an SPP.

We all received the pathetic letter from NAB chairman Michael Chaney yesterday who still doesn't appear to understand that he has presided over the largest dilution of retail shareholders we've seen in Australia this year.

Despite previously owning about 40% of the bank, retail investors have only provided $1 billion of new capital over the past 12 months whereas institutional investors have provided $5 billion and are now enjoying paper profits of about $1.8 billion.

I wrote to Mr Chaney on June 26, the day NAB announced it was spending $825 million buying Aviva, suggesting he launch another SPP to compensate small investors for the dilution from the $3.25 billion capital raising in December 2008 when retail investors only provided 7.7% or $250 million.

How did he respond? By launching another institutional placement and then further diluting retail investors by imposing the largest scaleback ever seen with an SPP.

Mr Chaney is up for re-election at NAB's 2009 AGM in December and I'll be running against him on a platform of providing a better deal for retail investors.

Stephen Mayne

Templestowe

The letter has caused some further email traffic and it will be very interesting to see how the issue plays out. With a full blown contested board election, our argument for the broader investing public probably needs to move on from the obscure theory of "dilution" and point out what the exercise really means: less dividends for small investors, less participation in the upside of a business they've owned and a complete lack of fairness. And if the directors are prepared to shaft retail shareholders on something so fundamental, what will they do next?

Finally, here are the other Mayne Report editions where this NAB scale back issue has been covered:

Come along tomorrow, Fairfax article, profit season, Business View, Australand looks good and NAB scandal

August 28, 2009

NAB shafting, capital raisings, pokies, council taxes, REA Group, Laker, Richies and much more

August 25, 2009

Manningham, bank bashing, capital raisings, Fairfax, Asciano, NAB, McCrann, Charlie Aitken, developers and much more

August 17, 2009

Terry McCrann keeps batting for small share holders

News Ltd's Terry McCrann has been the best of the commentators in recent months when it comes to standing up for small shareholders and you really should check out all four of his relevent columns:

No room at the trough for mums and dads

September 3, 2009

Asciano handout a winner

August 27

Boart sold on issue rip-off

August 18

Bendigo can screw them over like the big banks

August 11

The September 3 column got stuck into Skilled Engineering and Network Ten and the common feature in all these McCrann efforts has been railing against discounted institutional placements. Well done, Terry.

Time for other commentators to join McCrann campaign

Whilst The Age's Malcolm Maiden had this crack at NAB's share purchase plan, the business commentariat as a whole are yet to really wind up a decent campaign on retail dilution.

The two best business commentators, The Australian's John Durie and Business Spectator's Alan Kohler, have made the odd passing reference without ever really comprehensively dishing out the caning that the system deserves.

Kohler was an early mover, with this Speed Dating for Desperados column last December, but it only really focused on how investment banks were ripping off companies as a whole, rather than the issue of how different classes of shareholders were being treated. In May Kohler called in this column for independent directors to stand up and be counted on capital raisings but again there was no reference to retail dilution.

John Durie and his successor as The AFR's Chanticleer columnist, Alan Jury, have both been relatively subdued, so I sent them both an email last Thursday attempting to gee them up to wade in on the NAB dilution story. Fingers crossed something really substantial will eventually appear. John Durie did plug renounceable issues in today's column, but the big question is actually punishing the boards which rip-off retail investors and seeking some form of restitution. For instance, NAB should immediately launch another $5000 SPP at $21.50 and promise to leave it uncapped in a first move to fix the amazing shafting retail investors have copped.

Classic Cornwall - not about a John Durie column

The Virgin Blue scale back decision

Virgin Blue revealed last Thursday it was overwhelmed by retail investors seeking extra discounted shares in its 20c entitlement offer, but they are still pondering the scale back formula so I sent them the following email:

Subject: VBA scale back decision

Dear Heather, Keith and Brett,

After digesting today's announcement on VBA's entitlement offer, I'd like to make a suggestion on the specifics of your scale back decision.

Firstly, a disclosure: I've submitted applications for $23,000 in total for my wife and I but appreciate it would be unrealistic to expect a substantial allocation given we are both very small holders.

However, it would be good if you could allow those with unmarketable parcels to, at a minimum, get back above $500 worth of shares.

Given the Toll de-merger and poor share price performance, you have a lot of shareholders holding unmarketable parcels.

Therefore, can I suggest you adopt a scale back policy similar to Macquarie Leisure which allocated everyone $500 worth of additional shares and then offered 70% of entitlement up to the maximum $15,000. The MLE announcement is here:

Whilst some companies such as Alumina and DUET only go for an allocation of “overs” based on a multiple of entitlement, the vast majority had a minimum allocation such as the following:

Wesfarmers: $13,500

Onesteel: $36,000

Fairfax Media: $33,333

Santos: $62,500

It is important to be as transparent as possible about the scale back policy, so in your final announcement could you please disclose the total applications received and break it down into “overs” and “entitlement”. It would also be good to know how many shareholders applied for their entitlement and how many applies for “overs”.

Finally, congratulations for looking after the ineligible retail investors. VBA is the first company to do this all year.

I look forward to your reply and am available if you wish to discuss this further.

Regards, Stephen Mayne

Small VBA shareholder and very frequent Virgin Blue flyer

Commquest unravelling, Paris Hilton splurge signalled the end

As a staggering 284 companies released their 2008-09 earnings on Monday, August 31, the last day possible, it was interesting to note Melbourne-based marketing services company CommQuest attempted to hide its $52 million loss in the deluge.

Commquest is the outfit which paid Paris Hilton hundreds of thousands of dollars to attend a New Year's Eve party in 2008. We blew the lid on them in a story for Businessday on April 28 which had a staggering 255,000 page views in one day: Paris Hilton's $1m party tab for ANZ

There was plenty more in the April 30 and May 1 editions of The Mayne Report, including a gentle clip over the years for Amanda Gome and her Smart Company website which gave the Gen Y management team at CommQuest a very easy run.

Ironically, Smart Company is part of the Private Media Partners stable which is backed by Mark Carnegie and John Wylie from Lazard, the investment house which poured millions into CommQuest but is now suing claiming it was misled.

Fairfax reporter Dan Oakes noted Commquest's latest troubles with this story on September 2: Paris Hilton couldn't help CommQuest

Australand windfall as capital raising plays continue to deliver

The following list tracks the various capital raising plays we've completed in 2009 and those which are coming up. There's also this version ranking the biggest profits. Also, check out all trades in 2009 plus the full portfolio of more than 700 holdings worth less than $50,000.

It has been a good year playing the capital raisings in Australia and the gross profits have unfolded as follows on a monthly basis:

January: broke even

February: broke even

March: $10,170 profit

April: $36,996 profit

May: $31,639 profit

June: $86,600 profit

July: $28,293 profit

August: $12,758 profit

September: $7000 profit so far

Gross paper profits for year: $209,866

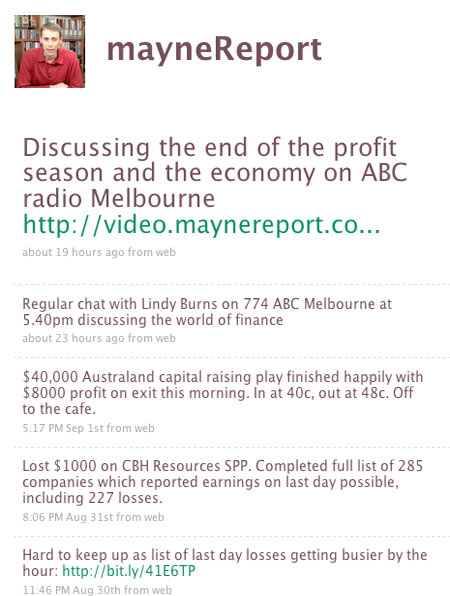

The three latest plays since the last edition have included our first substantial loss of $1000 on CBH Resources, but we bounced back the very next day with an $8000 gain on Australand so the positive trend seems to be continuing. Anyway, here's the detail since the August 28 edition:

August 31: put $38,000 into three NAB SPP offers but scaled back to 394 shares costsing $8471 and then exited for $28 to post a profit of $2500.

September 1

CBH Resources: put $15,000 into SPP at 10c and exited for average 9.4c to lose about $1000.

September 2

Australand: applied for maximum $40,000 into 40c entitlement offer and got full allocation. Exited at 48c to make profit of $8000.

Offers we're currently committed to

Amcor: $12,000 so far into entitlement offer at $4.30 which closes on Thursday.

Bendigo & Adelaide Bank: $30,000 into two entitlement offers at $6.75 which trade on September 17.

Energy & Minerals Australia: $2000 so far into SPP at 21c which closes today.

Goodman Group: $20,000 into two 1-for-1 entitlement offers at 40c which trade on September 17.

Intermoco: $10,000 into $15,000 SPP at 1.5c which trades later today.

Virgin Blue: $23,000 into 20c offer with unlimited ability to apply for extras which trades later this week.

Whitehaven Coal: $15,000 into SPP at $3.05 which trades later today.

Total live applications: $132,000

Woolworths push the grog shops in Manningham

Our very good friends at Woolworths are continuing their big push into grog and pokies in the city of Manningham.

Life as a local councillor involved a one hour meeting tonight with concerned residents near The Manningham Club in Bulleen, which is one of five pokies venues in our municipality owned by the joint venture giants of Woolworths and its colourful billionaire partner Bruce Mathieson.

The Manningham Club, which has had regulatory issues with claiming the tax concessions of being a club when in fact it is just run by the Woolworths-Mathieson joint venture company ALH, has appealed to VCAT after the council officers rejected its application to build a giant new bottle shop right up against the back fence of the residents. Given much of the site is a floodway it will be interesting to see what Melbourne Water thinks about all this.

Woolworths will no doubt wheel out the legal heavies to try and defeat the council and residents at VCAT but I for one am getting a little frustrated with its pattern of behaviour in Manningham.

Another resident who lives near the giant Shoppingtown Hotel on Manningham Road pointed out yesterday that the retail giant had long ago promised to remove the graffiti on its southern wall, but it remains there for the world to see.

And just a couple of kilometres further out down Doncaster Rd, Woolworths really upset the local traders at Jackson Court when it converted its Safeway into a giant Dan Murphy grog shop. Council responded by offering its car park for sale to a rival shopping centre developer and last week we announced ALDI had been appointed preferred developer as this article in our local paper explains.

Daryl Dixon and Max Walsh go the knuckle

Whilst The Mayne Report has long lamented the lack of institutional activism in corporate Australia, it has been very surprising to see two old stagers from the financial world, Daryl Dixon and Max Walsh, go the knuckle on a couple of listed investment companies in recent months.

Indeed the latest edition of Investment and Technology Magazine has a big feature on this lack of activism, whilst mentioning that a new fund Sandon Capital has entered the space.

The tussle between Dixon Advisory and van Eyk Three Pillars fund is getting very interesting.

In a nutshell Dixon Advisory are using the combined vote of their superannuation clients who hold about 35% of the van Eyk Three Pillars to make a bid for the board. The EGM will be held on September 29. But there's no takeover offer on the table. In short, it's a grab for the fees and Dixon Advisory sure do know how to charge every which way.

The van Eyk camp reckon they shouldn't be tossed out because the fund has delivered a gross dividend yield of 8.4% per annum since June 2004, compares favourably with its LIC peers, has resumed dividend payments and initiated a buyback strategy to try and reduce the discount to NTA - all of which happened before the hostile EGM was called.

Besides, two of the four directors are independent, including an independent chairman, whereas Dixon Advisory proposes to appoint all four directors. What about some independence and who will represent the 65% of minority shareholders? There's also the question of the fund losing its access to quality van Eyk Research

I was very surprised when Daryl Dixon rudely interrupted some fairly pedestrian questions to ANZ chairman Charles Goode at last year's Diversified United Investments AGM. Dixon came across as a stuffy old fellow who doesn't believe in any AGM interaction. Lo and behold, he suddenly launches a couple of expensive EGMs to remove entire boards with very little prior engagement. Strange days indeed.

The Walkley nomination

Nominations for the Walkley Awards closed last Friday and I've decided to enter for the third time in 20 years. The first entry - "AGM Season 1998" for The Daily Telegraph - was lobbed 10 years ago last Thursday and ended up winning the business category.

Crikey then nominated in 2002 after a series of scoops that caused the Democrats to implode and whilst we were finalists for the internet category, the Walkley went to 4 Corners.

Fast forward seven years and we've decided to have another crack. The entry is called "Educating the investing public by example" and the 400 word summary is as follows:

The three www.businessday.com.au online columns for this entry started with “How to make $75,000 in three months" on May 19 which attracted more than 250,000 page views in one day.

The follow up, “Get Rich quick – Part II” on June 3 attracted 160,000 page views whilst the fourth instalment, “Missing out on easy money” on June 23 had 80,000 page views.

Fairfax has never before had a three part business series collectively attract 490,000 page views and the opening column remains in the top 3 stories of all time for BusinessDay.

By the strength of these numbers and the subsequent change in behaviour by investors, it is clear these columns helped educate disenchanted or ill-informed small investors to start taking up profitable share offers.

This was an example of putting journalism ahead of personal financial interest. My personal situation would have been maximised by saying nothing and continuing to be an educated insider scooping up the shortfalls left by the likes of the 92% of Axa shareholders who in May declined to take up a share offer that was 30-40% in the money.

However, by telling the world through Australia's most popular business news website and also producing this list of all capital raising investments for The Mayne Report website, which has had more than 20,000 page views, investors were educated by example.

Without this series, Australian retail investors would have been hundreds of millions of dollars worse off, with the big end of town scooping up the benefit. I even had ASX chairman David Gonski tell me that his sister changed her investing practices after reading the columns.

The research was long and painstaking and was only possible from the decision to put together the world's biggest small share portfolio – 700 different tiny holdings – to assist with shareholder activism and journalistic research. This didn't come cheap, as by February this year I'd lost about $150,000 on the portfolio.

No other Australian journalist had access to the flow of offers during an unprecedented credit crunch when investors stumped up almost $100 billion. This was equivalent to about 10% of the entire market value, a level of new raisings unprecedented anywhere else in the world.

However, the system was chronically stacked against small investors and it was important to point this.

Record traffic for The Mayne Report

August 2009 was our biggest month yet for The Mayne Report. We had 137,261 page views and 87,679 unique visitors which equates to nearly 3000 visits a day. This is a big jump over our 2009 average of just over 50,000 visits per month at 1,648 per day.

August 7 was our biggest day with 17,151 page views and 9,496 visits. This can be directly attributed to this Fairfax article which was the seventh instalment of a series for Fairfax websites about how retail investors should play capital raisings.

Moreover, the Mayne Report video blog attracted 30,893 visitors in August. There was a spike of over 7,000 visitors on Friday, August 7 which relates to the Fairfax article on SPP plays, but it has grown to almost 1000 viewers a day.

Since we began recording stats for our videos beginning March 17, 2009, we have had 58,115 Absolute Unique Visitors and 233,481 pageviews. Our biggest day was May 19, 2009 with nearly 9,000 visitors, which can be attributed to this Fairfax article How to make $75,000 in three months.

Farewell to Telstra remuneration boss Charles Macek

Telstra's remuneration committee chairman Charles Macek has fallen on his sword and agreed not to stand for re-election at the AGM in November. The announcement was coupled with the appointment of two new directors. After the departure of Sol Trujillo this was an appropriate move given Charles was also one of the longest serving Telstra directors.

The public got a good look at Charles when he bravely engaged on executive pay through Jenny Brockie's excellent Insight debate program, as you can see from these edited highlights:

Meanwhile, two Mayne Report videos are going to be included in a forthcoming exhibition at the Australian Centre for the Moving Image inside Melbourne's Federation Square. We've been pondering which to offer up and for all those relatively new readers of this newsletter, our favourite four are at the top of our video site. Don't miss the video called Murdoch Muzzle - as it deals with the most outrageous dodging of question time we've even seen at an AGM.

2009 AGM season, AMP and more archive highlights

With a new AGM season almost upon us, we thought it was time to reflect on some past exchanges in this package of favourite AGM highlights. They are largely snappy 2-3 minute affairs and well worth a listen.

Additionally, here is a list of the record 66 AGMs we attended in 2008, plus links to the reports and audio. It will be hard work matching those numbers in 2009.

The AGM archive is being worked on regularly and this week it was AMP which came through with transcripts from the 2003 and 2009 AGMs.

The 2003 AMP tilt was the last for a couple of years after almost $10 billion in losses offshore still only produced a 19% vote against the responsible incumbent directors and a mammoth 89% vote against your correspondent.

The lively events were captured in Crikey at the time, the results are here, but now we've also got the full transcript, which has been edited down to these highlights. A personal favourite was an old chap Mr Lauriston explaining why the outside candidate wouldn't get his vote:

Mr Lauriston: I am going to support everyone who is up for election except Mr Mayne....Mr Mayne is a very courageous, very intelligent, very well educated gentleman. In my opinion he is scrupulously honest. I will repeat that, he is scrupulously honest. He is a very lovable fellow, but the poor man couldn't run a two-bob chook raffle at the RSL. Sorry.

The 2009 AMP AGM was also pretty lively as you can from the edited transcript. Watch the Meredith Hellicar spray here and check out the edited webcast of our questions here.

Press Room and podcasts

Below are this weeks contributions:

Businessday.com.au

Elders caps worst earnings year on record

September 4, 2009

Crikey

Will Kirk's $4 million farewell be the end of Ron Walker?

September 4, 2009

Kennett, Bracks, Jeffed — it's 10th anniversary season

September 3, 2009

Fourteen join the billion dollar loss club

September 1, 2009

Profit season's last day dross and $1 billion loss

August 31, 2009

Radio

774 ABC Melbourne - discussing the results season and the economy. Wednesday, September 2.

774 ABC Melbourne - discussing emissions trading, state of the economy and James Hardie. Wednesday, August 26

Click the link to get the latest radio and AGM audio.

Classic Cornwall

The Mayne Report Rich List

Since we began compiling the Mayne Report Rich List documenting every Australian currently or previously worth more then $10 million, it has grown in numbers and popularity such that no other feature on our website can match it for traffic.

We're now up to 1375 entries, although some are italicised, denoting that they are no longer worth more than our $10 million cut off. Send us through any tips or suggestions of anyone you think deserves a spot on the list. The dramatic Woolworths move into hardware has today created the following new entry:

Updated entry - Alstergren family: founded by Edvaad Alstergren, of Norway. He came to Australia as an immigrant, married an Australian, Marjorie, had seven children and made a fortune in timber. When he died, the company, which included Softwoods Holdings and Timber Holdings, Timber Holdings Tasmania were taken over by CSR.

Mark Bethwaite: a former Liberal Party federal treasurer and Australian Olympic Sailing Team member at three Olympics. He competed at Munich in 1972, Montreal in 1976 and Moscow in 1980. In 2007 he sold his humble Mosman waterfront cottage to the chief doctor from Primary Healthcare, Ed Bateman, for a reported $13.5 million. This wealth was largely assembled from his time as an executive director of the old North Broken Hill.

Mayne Report RSS Feeds

The Mayne Report now has RSS feeds for you. We have bundled our best articles into a simple and easy delivery for you. Add an RSS feed to your personal reader, iGoogle, MyYahoo, or blog. It's quick and easy to do and means you're always up to date with the latest Mayne Report activity.

More Cornwall cartoons for The Mayne Report

Former Fairfax and Crikey cartoonist Mark Cornwall has been contributing his satirical commentary to the Mayne Report since March 2009. Here is a collection of his best cartoons and there are now some amusing animations he has begun. Go here to see his animations and below are some new offerings:

Sign up for Mayne Report Tweets

We have only been twittering for a few months, but now have 676 followers and are regularly dropping out the latest developments from AGMs, capital raising plays and even Manningham Council. Sign up below to get the latest updates from all our activity and check out some of the latest tweets :

That's all for now.

Do ya best, Stephen Mayne

* The Mayne Report is a multi-media governance website published by Stephen Mayne with occasional email editions. To unsubscribe from the emails click here.

apologies it was 11 days between editions but we hope you'll think it was worth the wait.

Staggering 52 companies join $100 million loss club

When a record 29 ASX-listed companies reported losses of more than $100 million in 2007-08, we thought it was pretty remarkable. Amazingly, the 2008-09 season delivered unprecedented amounts of red ink, caused by the global financial crisis, with losses of more than $100 million for a record 52 companies. That's a pretty amazing statistic given that we had previously only found 75 companies that had achieved this unfortunate milestone more than 150 times over the past 20 years.

Check out where these latest losses sit in the all-time list tracking $100 million losses from biggest to smallest.

It has been a very interesting process tracking the timing of earnings results. For instance, check out this list to see when the 52 $100m-plus losses were announced. Surprise, surprise they were heavily weighted towards the last few days of the reporting season.

We gave the issue a big burst on the Fairfax websites last Friday just ahead of Elders releasing their season-ending $414 million net loss.

And check out this amazing chronological list of how 285 companies dropped their results on the last possible day.

Elders shaft big retail investors like never before

The $550 million emergency Elders capital raising has been generating plenty of press and the company comes in at number 37 on our new mega-list tracking all major capital raisings since the beginning of 2008.

The monster placement of new shares at a miserable 15c a pop surpasses even the Asciano record for retail dilution. At least with Asciano retail investors had a 1-for-1 entitlement offer and were able to apply for 2.1 times their entitlement, followed by a $10,000 share purchase plan, albeit scaled back by 65% in the end.

Asciano started the process with 700 million shares on issue and then did a placement of 2.137 billion shares - more than three times the existing capital base when the law limits companies to issuing just 15% of shares by way of placement in any 12 month period without shareholder approval.

Elders shares last traded at 39c before the capital raising and with 818 million shares on issue this capitalised the business at $319 million.

However, after all this talk of a straightforward 25c renounceable rights issue, the company came back with a whopping $400 million institutional placement that comprised issuing 2.667 billion new shares at 15c - equivalent to 3.26 times the original number of shares. Whilst there is no pro-rata entitlement offer at all, the sop to retail investors is a $150 million share purchase plan with each Australian and New Zealand investor entitled to buy up 133,333 shares at 15c each for a total of $20,000, a figure we've never seen before with an SPP.

Whilst our family are likely to be big winners from all this, the following email exchange with a sophisticated retail investor, who we'll call Warren, sums up the key problems and themes:

Warren to Mayne Report

Hi Stephen,

Disgraceful and unashamed dilution of the larger retail holders at Elders, but great for small holders like yourself assuming you get the full $20,000. What's wrong with a fully renounceable rights issue? They had some momentum but chose to give all the upside to the instos.

Will be an interesting one to dissect.

All the best, Warren

Mayne Report to Warren

I agree, amazing windfall for tiny holders, huge shafting of bigger holders. It seems refusal of biggest shareholder to participate, some UK insto with 15%, led to decision to shaft them big time.

The wife and I are both in there so windfall on tonight's close is $25,000 although the maximum uptake assuming all 32,000 shareholders participate is $640 million so likely to be scale back which they would have to skew in favour of larger retail.

My tip would be something like everyone with more than 10,000 shares gets full allocation, the rest get scaled back with a minimum allocation of perhaps $5000 to the smallest such as myself.

Anyway, time will tell but I'll write this up during the week.

Cheers, Stephen

Warren to Mayne Report

I'm OK I only hold the hybrids, which is a mixed blessing, on the one hand the risk of losing the lot is now minimal but they have suspended the dividend for 2 years and scotched the dividend on the ordinary shares for almost 3 years as collateral damage.

For the life of me I can't understand why they suspended the hybrid dividends, why would they offer it up to the debt holders? I obviously don't understand fully the re-financing but from what I can see nobody holding their debt took a haircut. As long they keep making their interest payments and stay within their covenants what comfort would not paying the hybrids give the debt holders?

Anyway the EGM will be pretty colourful, I half expect some disgruntled cockies who have held long term to turn up on horseback dressed as Ned Kelly.

Good luck to you and Paula

Mayne Report to Warren

What's the coupon on the hybrid? There's 1.5 million outstanding at $100 presumably so what's it going to save them?

Also, is it repayment at par in 2011? If so, that would be a screaming buy once shareholders approve placement/SPP given reduction in risk.

Hybrids were a big factor in collapse of Babcock & Brown and will be a major factor in recapitalisation proposal for Babcock & Brown Infrastructure. Save from putting the company under, it seems the worst they can do is suspend coupons until maturity.

Cheers, Stephen

Warren to Mayne Report

Coupon is currently bank bill swap rate plus 2.2% and will step up another 2.5% in 2011.

So I guess it is currently about $7–8m per annum, not going to drive them to the wall but not insubstantial. I guess I don't understand why they would say 2 years. The payment of the hybrid dividend is at the discretion of the directors, why limit themselves with this kind condition, if the business is going gang busters in 12 months what then? Surely would be more prudent to consider as a quarter to quarter proposition (which I reckon was the original intent of the issue). As I said if they are getting paid and the business is trading within the covenants why would the other debt holders care?

Unfortunately the hybrids are perpetual – the thinking is that 4.7% over BBSW (after step up) would probably incent the company to redeem. I guess a cynic might question this in the light of the current suspension of dividends.

Given that they have cleared the decks in terms of debt and non-core businesses the more likely trigger for redemption is a takeover. With the new look balance sheet I reckon they will be in play in the next 12 months? Dare I use the term LBO?

The trip to Adelaide for the Elders EGM on October 15 would ordinarily be a no brainer, but unfortunately it clashes with a speaking commitment at a big capital raising conference in Sydney, so if anyone fancies being the proxy, drop us a line to stephen@maynereport.com.

Contested election for NAB chairman Michael Chaney

The National Australia Bank SPP scale back scandal is starting to get a bit more mainstream media traction. Michael Pascoe powerfully called for NAB chairman Michael Chaney to be booted off the board in his end of week video for Fairfax two Friday's back and 4BC Drive presenter Mike Smith was happy to stick the boot in during this interview with your correspondent on the same day.

NAB has clearly been inundated by complaints from irate shareholders based on this letter its chairman sent out with the refund and allotment notices last week. Chaney opened up with the following:

Dear Shareholder, there has been a great deal of discussion and comment in recent days on institutional share placements and Share

Purchase Plans.

Well, not really. The AFR's letters pages have carried some debate but the top business columnists have largely been missing in action. The whole point of rushing out this edition of The Mayne Report on August 25 was to alert the mainstream media to the scandal, but it literally generated only a couple of paragraphs in The AFR on August 26.

It's not often more than 150,000 Australians get collectively shafted out of $300 million but that's what NAB did and these retail investors are clearly fuming.

The Chaney letter did trigger a page lead in The AFR last Thursday, but it contained an error so the following letter was fired off by your correspondent which was finally published in yesterday's paper as follows:

NAB's miserable 202 shares from SPP

Matthew Drummond's story (“Chaney tries to soothe NAB shareholders”, September 3) about National Australia Bank's share purchase plan claims “the maximum allotment will be $15,000”.

If only it were so. The problem with NAB is that it has slashed more than 150,000 shareholders who applied for the full $15,000 allotment down to a miserable 202 shares costing $4343.

Investors are rightly up in arms about this 71% scale back. They didn't want to collectively receive $1.85 billion in refunds, especially when no other Australian bank has ever scaled back an SPP.

We all received the pathetic letter from NAB chairman Michael Chaney yesterday who still doesn't appear to understand that he has presided over the largest dilution of retail shareholders we've seen in Australia this year.

Despite previously owning about 40% of the bank, retail investors have only provided $1 billion of new capital over the past 12 months whereas institutional investors have provided $5 billion and are now enjoying paper profits of about $1.8 billion.

I wrote to Mr Chaney on June 26, the day NAB announced it was spending $825 million buying Aviva, suggesting he launch another SPP to compensate small investors for the dilution from the $3.25 billion capital raising in December 2008 when retail investors only provided 7.7% or $250 million.

How did he respond? By launching another institutional placement and then further diluting retail investors by imposing the largest scaleback ever seen with an SPP.

Mr Chaney is up for re-election at NAB's 2009 AGM in December and I'll be running against him on a platform of providing a better deal for retail investors.

Stephen Mayne

Templestowe

The letter has caused some further email traffic and it will be very interesting to see how the issue plays out. With a full blown contested board election, our argument for the broader investing public probably needs to move on from the obscure theory of "dilution" and point out what the exercise really means: less dividends for small investors, less participation in the upside of a business they've owned and a complete lack of fairness. And if the directors are prepared to shaft retail shareholders on something so fundamental, what will they do next?

Finally, here are the other Mayne Report editions where this NAB scale back issue has been covered:

Come along tomorrow, Fairfax article, profit season, Business View, Australand looks good and NAB scandal

August 28, 2009

NAB shafting, capital raisings, pokies, council taxes, REA Group, Laker, Richies and much more

August 25, 2009

Manningham, bank bashing, capital raisings, Fairfax, Asciano, NAB, McCrann, Charlie Aitken, developers and much more

August 17, 2009

Terry McCrann keeps batting for small share holders

News Ltd's Terry McCrann has been the best of the commentators in recent months when it comes to standing up for small shareholders and you really should check out all four of his relevent columns:

No room at the trough for mums and dads

September 3, 2009

Asciano handout a winner

August 27

Boart sold on issue rip-off

August 18

Bendigo can screw them over like the big banks

August 11

The September 3 column got stuck into Skilled Engineering and Network Ten and the common feature in all these McCrann efforts has been railing against discounted institutional placements. Well done, Terry.

Time for other commentators to join McCrann campaign

Whilst The Age's Malcolm Maiden had this crack at NAB's share purchase plan, the business commentariat as a whole are yet to really wind up a decent campaign on retail dilution.

The two best business commentators, The Australian's John Durie and Business Spectator's Alan Kohler, have made the odd passing reference without ever really comprehensively dishing out the caning that the system deserves.

Kohler was an early mover, with this Speed Dating for Desperados column last December, but it only really focused on how investment banks were ripping off companies as a whole, rather than the issue of how different classes of shareholders were being treated. In May Kohler called in this column for independent directors to stand up and be counted on capital raisings but again there was no reference to retail dilution.

John Durie and his successor as The AFR's Chanticleer columnist, Alan Jury, have both been relatively subdued, so I sent them both an email last Thursday attempting to gee them up to wade in on the NAB dilution story. Fingers crossed something really substantial will eventually appear. John Durie did plug renounceable issues in today's column, but the big question is actually punishing the boards which rip-off retail investors and seeking some form of restitution. For instance, NAB should immediately launch another $5000 SPP at $21.50 and promise to leave it uncapped in a first move to fix the amazing shafting retail investors have copped.

Classic Cornwall - not about a John Durie column

The Virgin Blue scale back decision

Virgin Blue revealed last Thursday it was overwhelmed by retail investors seeking extra discounted shares in its 20c entitlement offer, but they are still pondering the scale back formula so I sent them the following email:

Subject: VBA scale back decision

Dear Heather, Keith and Brett,

After digesting today's announcement on VBA's entitlement offer, I'd like to make a suggestion on the specifics of your scale back decision.

Firstly, a disclosure: I've submitted applications for $23,000 in total for my wife and I but appreciate it would be unrealistic to expect a substantial allocation given we are both very small holders.

However, it would be good if you could allow those with unmarketable parcels to, at a minimum, get back above $500 worth of shares.

Given the Toll de-merger and poor share price performance, you have a lot of shareholders holding unmarketable parcels.

Therefore, can I suggest you adopt a scale back policy similar to Macquarie Leisure which allocated everyone $500 worth of additional shares and then offered 70% of entitlement up to the maximum $15,000. The MLE announcement is here:

Whilst some companies such as Alumina and DUET only go for an allocation of “overs” based on a multiple of entitlement, the vast majority had a minimum allocation such as the following:

Wesfarmers: $13,500

Onesteel: $36,000

Fairfax Media: $33,333

Santos: $62,500

It is important to be as transparent as possible about the scale back policy, so in your final announcement could you please disclose the total applications received and break it down into “overs” and “entitlement”. It would also be good to know how many shareholders applied for their entitlement and how many applies for “overs”.

Finally, congratulations for looking after the ineligible retail investors. VBA is the first company to do this all year.

I look forward to your reply and am available if you wish to discuss this further.

Regards, Stephen Mayne

Small VBA shareholder and very frequent Virgin Blue flyer

Commquest unravelling, Paris Hilton splurge signalled the end

As a staggering 284 companies released their 2008-09 earnings on Monday, August 31, the last day possible, it was interesting to note Melbourne-based marketing services company CommQuest attempted to hide its $52 million loss in the deluge.

Commquest is the outfit which paid Paris Hilton hundreds of thousands of dollars to attend a New Year's Eve party in 2008. We blew the lid on them in a story for Businessday on April 28 which had a staggering 255,000 page views in one day: Paris Hilton's $1m party tab for ANZ

There was plenty more in the April 30 and May 1 editions of The Mayne Report, including a gentle clip over the years for Amanda Gome and her Smart Company website which gave the Gen Y management team at CommQuest a very easy run.

Ironically, Smart Company is part of the Private Media Partners stable which is backed by Mark Carnegie and John Wylie from Lazard, the investment house which poured millions into CommQuest but is now suing claiming it was misled.

Fairfax reporter Dan Oakes noted Commquest's latest troubles with this story on September 2: Paris Hilton couldn't help CommQuest

Australand windfall as capital raising plays continue to deliver

The following list tracks the various capital raising plays we've completed in 2009 and those which are coming up. There's also this version ranking the biggest profits. Also, check out all trades in 2009 plus the full portfolio of more than 700 holdings worth less than $50,000.

It has been a good year playing the capital raisings in Australia and the gross profits have unfolded as follows on a monthly basis:

January: broke even

February: broke even

March: $10,170 profit

April: $36,996 profit

May: $31,639 profit

June: $86,600 profit

July: $28,293 profit

August: $12,758 profit

September: $7000 profit so far

Gross paper profits for year: $209,866

The three latest plays since the last edition have included our first substantial loss of $1000 on CBH Resources, but we bounced back the very next day with an $8000 gain on Australand so the positive trend seems to be continuing. Anyway, here's the detail since the August 28 edition:

August 31: put $38,000 into three NAB SPP offers but scaled back to 394 shares costsing $8471 and then exited for $28 to post a profit of $2500.

September 1

CBH Resources: put $15,000 into SPP at 10c and exited for average 9.4c to lose about $1000.

September 2

Australand: applied for maximum $40,000 into 40c entitlement offer and got full allocation. Exited at 48c to make profit of $8000.

Offers we're currently committed to

Amcor: $12,000 so far into entitlement offer at $4.30 which closes on Thursday.

Bendigo & Adelaide Bank: $30,000 into two entitlement offers at $6.75 which trade on September 17.

Energy & Minerals Australia: $2000 so far into SPP at 21c which closes today.

Goodman Group: $20,000 into two 1-for-1 entitlement offers at 40c which trade on September 17.

Intermoco: $10,000 into $15,000 SPP at 1.5c which trades later today.

Virgin Blue: $23,000 into 20c offer with unlimited ability to apply for extras which trades later this week.

Whitehaven Coal: $15,000 into SPP at $3.05 which trades later today.

Total live applications: $132,000

Woolworths push the grog shops in Manningham

Our very good friends at Woolworths are continuing their big push into grog and pokies in the city of Manningham.

Life as a local councillor involved a one hour meeting tonight with concerned residents near The Manningham Club in Bulleen, which is one of five pokies venues in our municipality owned by the joint venture giants of Woolworths and its colourful billionaire partner Bruce Mathieson.

The Manningham Club, which has had regulatory issues with claiming the tax concessions of being a club when in fact it is just run by the Woolworths-Mathieson joint venture company ALH, has appealed to VCAT after the council officers rejected its application to build a giant new bottle shop right up against the back fence of the residents. Given much of the site is a floodway it will be interesting to see what Melbourne Water thinks about all this.

Woolworths will no doubt wheel out the legal heavies to try and defeat the council and residents at VCAT but I for one am getting a little frustrated with its pattern of behaviour in Manningham.

Another resident who lives near the giant Shoppingtown Hotel on Manningham Road pointed out yesterday that the retail giant had long ago promised to remove the graffiti on its southern wall, but it remains there for the world to see.

And just a couple of kilometres further out down Doncaster Rd, Woolworths really upset the local traders at Jackson Court when it converted its Safeway into a giant Dan Murphy grog shop. Council responded by offering its car park for sale to a rival shopping centre developer and last week we announced ALDI had been appointed preferred developer as this article in our local paper explains.

Daryl Dixon and Max Walsh go the knuckle

Whilst The Mayne Report has long lamented the lack of institutional activism in corporate Australia, it has been very surprising to see two old stagers from the financial world, Daryl Dixon and Max Walsh, go the knuckle on a couple of listed investment companies in recent months.

Indeed the latest edition of Investment and Technology Magazine has a big feature on this lack of activism, whilst mentioning that a new fund Sandon Capital has entered the space.

The tussle between Dixon Advisory and van Eyk Three Pillars fund is getting very interesting.

In a nutshell Dixon Advisory are using the combined vote of their superannuation clients who hold about 35% of the van Eyk Three Pillars to make a bid for the board. The EGM will be held on September 29. But there's no takeover offer on the table. In short, it's a grab for the fees and Dixon Advisory sure do know how to charge every which way.

The van Eyk camp reckon they shouldn't be tossed out because the fund has delivered a gross dividend yield of 8.4% per annum since June 2004, compares favourably with its LIC peers, has resumed dividend payments and initiated a buyback strategy to try and reduce the discount to NTA - all of which happened before the hostile EGM was called.

Besides, two of the four directors are independent, including an independent chairman, whereas Dixon Advisory proposes to appoint all four directors. What about some independence and who will represent the 65% of minority shareholders? There's also the question of the fund losing its access to quality van Eyk Research

I was very surprised when Daryl Dixon rudely interrupted some fairly pedestrian questions to ANZ chairman Charles Goode at last year's Diversified United Investments AGM. Dixon came across as a stuffy old fellow who doesn't believe in any AGM interaction. Lo and behold, he suddenly launches a couple of expensive EGMs to remove entire boards with very little prior engagement. Strange days indeed.

The Walkley nomination

Nominations for the Walkley Awards closed last Friday and I've decided to enter for the third time in 20 years. The first entry - "AGM Season 1998" for The Daily Telegraph - was lobbed 10 years ago last Thursday and ended up winning the business category.

Crikey then nominated in 2002 after a series of scoops that caused the Democrats to implode and whilst we were finalists for the internet category, the Walkley went to 4 Corners.

Fast forward seven years and we've decided to have another crack. The entry is called "Educating the investing public by example" and the 400 word summary is as follows:

The three www.businessday.com.au online columns for this entry started with “How to make $75,000 in three months" on May 19 which attracted more than 250,000 page views in one day.

The follow up, “Get Rich quick – Part II” on June 3 attracted 160,000 page views whilst the fourth instalment, “Missing out on easy money” on June 23 had 80,000 page views.

Fairfax has never before had a three part business series collectively attract 490,000 page views and the opening column remains in the top 3 stories of all time for BusinessDay.

By the strength of these numbers and the subsequent change in behaviour by investors, it is clear these columns helped educate disenchanted or ill-informed small investors to start taking up profitable share offers.

This was an example of putting journalism ahead of personal financial interest. My personal situation would have been maximised by saying nothing and continuing to be an educated insider scooping up the shortfalls left by the likes of the 92% of Axa shareholders who in May declined to take up a share offer that was 30-40% in the money.

However, by telling the world through Australia's most popular business news website and also producing this list of all capital raising investments for The Mayne Report website, which has had more than 20,000 page views, investors were educated by example.

Without this series, Australian retail investors would have been hundreds of millions of dollars worse off, with the big end of town scooping up the benefit. I even had ASX chairman David Gonski tell me that his sister changed her investing practices after reading the columns.

The research was long and painstaking and was only possible from the decision to put together the world's biggest small share portfolio – 700 different tiny holdings – to assist with shareholder activism and journalistic research. This didn't come cheap, as by February this year I'd lost about $150,000 on the portfolio.

No other Australian journalist had access to the flow of offers during an unprecedented credit crunch when investors stumped up almost $100 billion. This was equivalent to about 10% of the entire market value, a level of new raisings unprecedented anywhere else in the world.

However, the system was chronically stacked against small investors and it was important to point this.

Record traffic for The Mayne Report

August 2009 was our biggest month yet for The Mayne Report. We had 137,261 page views and 87,679 unique visitors which equates to nearly 3000 visits a day. This is a big jump over our 2009 average of just over 50,000 visits per month at 1,648 per day.

August 7 was our biggest day with 17,151 page views and 9,496 visits. This can be directly attributed to this Fairfax article which was the seventh instalment of a series for Fairfax websites about how retail investors should play capital raisings.

Moreover, the Mayne Report video blog attracted 30,893 visitors in August. There was a spike of over 7,000 visitors on Friday, August 7 which relates to the Fairfax article on SPP plays, but it has grown to almost 1000 viewers a day.

Since we began recording stats for our videos beginning March 17, 2009, we have had 58,115 Absolute Unique Visitors and 233,481 pageviews. Our biggest day was May 19, 2009 with nearly 9,000 visitors, which can be attributed to this Fairfax article How to make $75,000 in three months.

Farewell to Telstra remuneration boss Charles Macek

Telstra's remuneration committee chairman Charles Macek has fallen on his sword and agreed not to stand for re-election at the AGM in November. The announcement was coupled with the appointment of two new directors. After the departure of Sol Trujillo this was an appropriate move given Charles was also one of the longest serving Telstra directors.

The public got a good look at Charles when he bravely engaged on executive pay through Jenny Brockie's excellent Insight debate program, as you can see from these edited highlights:

Meanwhile, two Mayne Report videos are going to be included in a forthcoming exhibition at the Australian Centre for the Moving Image inside Melbourne's Federation Square. We've been pondering which to offer up and for all those relatively new readers of this newsletter, our favourite four are at the top of our video site. Don't miss the video called Murdoch Muzzle - as it deals with the most outrageous dodging of question time we've even seen at an AGM.

2009 AGM season, AMP and more archive highlights

With a new AGM season almost upon us, we thought it was time to reflect on some past exchanges in this package of favourite AGM highlights. They are largely snappy 2-3 minute affairs and well worth a listen.

Additionally, here is a list of the record 66 AGMs we attended in 2008, plus links to the reports and audio. It will be hard work matching those numbers in 2009.

The AGM archive is being worked on regularly and this week it was AMP which came through with transcripts from the 2003 and 2009 AGMs.

The 2003 AMP tilt was the last for a couple of years after almost $10 billion in losses offshore still only produced a 19% vote against the responsible incumbent directors and a mammoth 89% vote against your correspondent.

The lively events were captured in Crikey at the time, the results are here, but now we've also got the full transcript, which has been edited down to these highlights. A personal favourite was an old chap Mr Lauriston explaining why the outside candidate wouldn't get his vote:

Mr Lauriston: I am going to support everyone who is up for election except Mr Mayne....Mr Mayne is a very courageous, very intelligent, very well educated gentleman. In my opinion he is scrupulously honest. I will repeat that, he is scrupulously honest. He is a very lovable fellow, but the poor man couldn't run a two-bob chook raffle at the RSL. Sorry.

The 2009 AMP AGM was also pretty lively as you can from the edited transcript. Watch the Meredith Hellicar spray here and check out the edited webcast of our questions here.

Press Room and podcasts

Below are this weeks contributions:

Businessday.com.au

Elders caps worst earnings year on record

September 4, 2009

Crikey

Will Kirk's $4 million farewell be the end of Ron Walker?

September 4, 2009

Kennett, Bracks, Jeffed — it's 10th anniversary season

September 3, 2009

Fourteen join the billion dollar loss club

September 1, 2009

Profit season's last day dross and $1 billion loss

August 31, 2009

Radio

774 ABC Melbourne - discussing the results season and the economy. Wednesday, September 2.

774 ABC Melbourne - discussing emissions trading, state of the economy and James Hardie. Wednesday, August 26

Click the link to get the latest radio and AGM audio.

Classic Cornwall

The Mayne Report Rich List

Since we began compiling the Mayne Report Rich List documenting every Australian currently or previously worth more then $10 million, it has grown in numbers and popularity such that no other feature on our website can match it for traffic.

We're now up to 1375 entries, although some are italicised, denoting that they are no longer worth more than our $10 million cut off. Send us through any tips or suggestions of anyone you think deserves a spot on the list. The dramatic Woolworths move into hardware has today created the following new entry:

Updated entry - Alstergren family: founded by Edvaad Alstergren, of Norway. He came to Australia as an immigrant, married an Australian, Marjorie, had seven children and made a fortune in timber. When he died, the company, which included Softwoods Holdings and Timber Holdings, Timber Holdings Tasmania were taken over by CSR.

Mark Bethwaite: a former Liberal Party federal treasurer and Australian Olympic Sailing Team member at three Olympics. He competed at Munich in 1972, Montreal in 1976 and Moscow in 1980. In 2007 he sold his humble Mosman waterfront cottage to the chief doctor from Primary Healthcare, Ed Bateman, for a reported $13.5 million. This wealth was largely assembled from his time as an executive director of the old North Broken Hill.

Mayne Report RSS Feeds

The Mayne Report now has RSS feeds for you. We have bundled our best articles into a simple and easy delivery for you. Add an RSS feed to your personal reader, iGoogle, MyYahoo, or blog. It's quick and easy to do and means you're always up to date with the latest Mayne Report activity.

More Cornwall cartoons for The Mayne Report

Former Fairfax and Crikey cartoonist Mark Cornwall has been contributing his satirical commentary to the Mayne Report since March 2009. Here is a collection of his best cartoons and there are now some amusing animations he has begun. Go here to see his animations and below are some new offerings:

Sign up for Mayne Report Tweets

We have only been twittering for a few months, but now have 676 followers and are regularly dropping out the latest developments from AGMs, capital raising plays and even Manningham Council. Sign up below to get the latest updates from all our activity and check out some of the latest tweets :

That's all for now.

Do ya best, Stephen Mayne

* The Mayne Report is a multi-media governance website published by Stephen Mayne with occasional email editions. To unsubscribe from the emails click here.